While the conventional wisdom around blockchain is that it’s a technology only affecting financial markets, design and construction stakeholders ought to pay attention to new developments, too. If you don’t, you risk falling behind on an important trend that potentially presents a competitive challenge for your firm.

You also risk missing the opportunity the technology itself presents. Blockchain and its real-world applications are constantly evolving—which is why understanding the basics now is so critical.

With that in mind, here are the five things you need to know now about blockchain.

- At the core, it’s just a database.

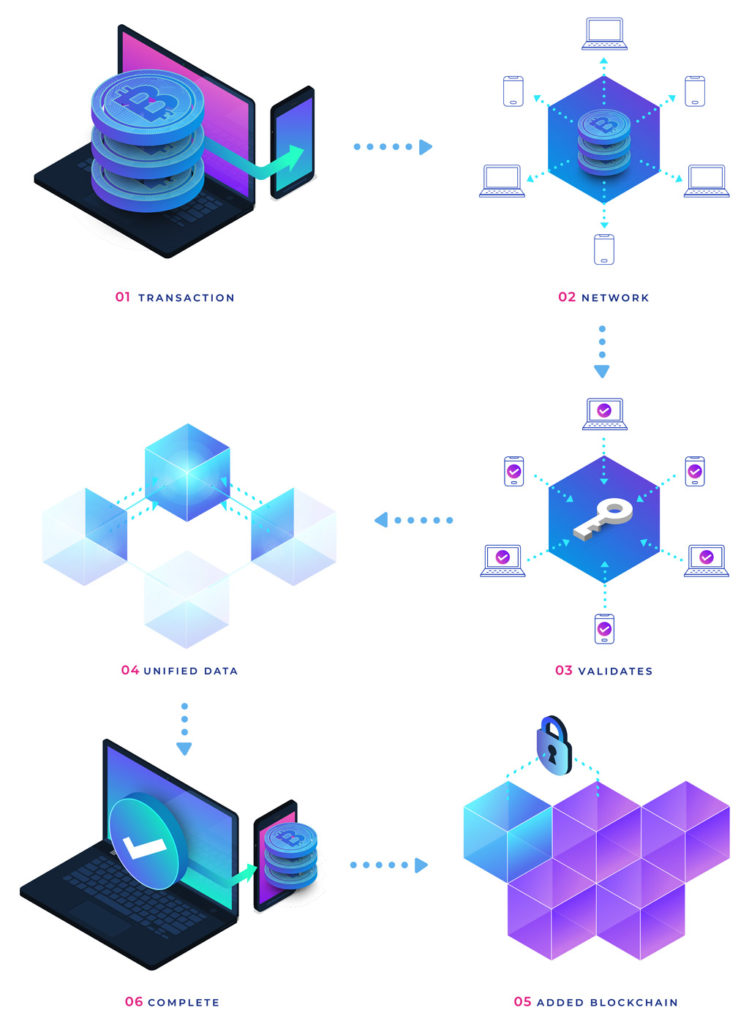

If you Google blockchain or ask a technologist what it is, you’ll get a slew of technical responses like “global ledger,” “distributed ledger technology,” “mining,” or “immutable record.” However, when you filter through all the technical explanations, blockchain technology is just a database.

Granted, it has special design features that make it groundbreaking: It changes the base layer of the internet’s infrastructure to help people secure their identities. It does this by pairing a public and a private key that enables one-way encryption and decryption but that’s all you really need to know about the technical aspect of blockchain.

- It helps get the upper hand on hackers by decentralizing and distributing risk.

Unlike traditional databases, where one party controls the data or information in the database, blockchain technology is a decentralized transaction ecosystem where multiple parties to the database (or network) contribute transactional data in real-time and all have a complete copy of the latest version as well as the history of previous versions. Access is decentralized and the risk is distributed so that no single party carries the risk of a breach. Thus, hackers can’t hold data or records ransom, for example, because all parties have a full and complete copy of the database and its history.

In this transaction ecosystem, architectural services, engineering services, legal services, and construction services all can be transacted over the internet. That makes blockchain applicable and valuable, not just to financial services, but to all commerce—including your own.

- It eliminates the middle man.

Blockchain enables true digitization, where agreements to provide services are digitized with tokens (that can represent USD or other assets) and those tokens can be transferred through the internet without needing intermediaries to process or verify the transaction. Unlike traditional transactions where a bank, credit card company, or other intermediary is required to verify and validate the release of the ‘thing of value,’ blockchain-based transactions are processed using an algorithm through a decentralized network of computers.

For example, in a neighborhood where homeowners have rooftop solar panels and one homeowner produces more energy than needed, blockchain technology cuts out the middle man (i.e. the utility) and enables homeowners to sell their excess generated energy in real-time to a neighbor. In fact, this scenario is playing out in a pilot project in Brooklyn.

The medical industry is also neck-deep in blockchain pilot projects relating to “womb to tomb” medical records, with the aim to break down the silos in medical record-keeping, giving patients the power to securely manage their health records, and ultimately deploy holistic care. With blockchain technology, an infant’s birth is recorded in a digital, blockchain-based record; all subsequent health care treatment is recorded in the same digital record for that person’s entire life. Access to health care history is provided by the patient who gives access to the provider through a private, cryptographic key. With this use case, gone would be the days that patients have to recollect from memory (or a paper file) their medical history for future health care providers’ use.

- It’s getting big attention in statehouses across the country.

Already in 2018, 14 state legislatures (Arizona, California, Colorado, Connecticut, Illinois, Maryland, Missouri, Nebraska, New Jersey, New York, Tennessee, Vermont, Virginia, and Wyoming) are currently considering or are in the process of passing legislation related to blockchain or its potential applications. Most of this legislation explicitly enables blockchain technology (albeit not necessarily required), mandates agencies to explore the technology, or formally institutes the study of the technology for use. Compared to last year when only seven state legislatures were actively exploring legislation and just three in 2016, this year’s uptick is an indicator of a trend that will likely continue to grow.

- The design and construction industry is ripe for the transformational change blockchain represents.

Several potential use cases connect blockchain to the design and construction industry. No other industry needs better, more efficient ways to collaborate and transact. Projects of all sizes involve multiple stakeholders and phases from financing and funding to planning to design and, finally, to construction, maintenance, and operations. How might blockchain bridge communications between so many stakeholders and streamline this complex process?

One particular area to watch is smart contract technology. Smart contracts are self-enforcing contracts enabled with blockchain technology. What’s interesting about this application is that it behaves as a governing mechanism of the relationships between the parties, similar to a traditional contract, but also as governance-on-wheels because the terms and conditions are connected to the flow of funds and aids in automating a sequence of events. It’s an active, self-enforcing contract that is automated through a series of coded if/then statements—in other words, an automated contract.

In its simplest form, a smart contract operates like a vending machine: You put money in, get the good of your choice, get your change, and the machine itself is designed to be secure in that the effort required to break into it isn’t worth the amount of money it’s designed to hold.

In a more complex transactional environment such as the design/construction industry, you can imagine breaking down a more traditional contract for design and construction services into a series of actions that are connected to payments. So, the governance document not only governs the agreement for services between the parties, but also self-executes on payments and acts as a project management platform all in one. For example, if service X is provided, then payment X-1 is made automatically and service Y is notified that work can begin. The question isn’t whether smart contracts are coming to the design and construction industry, but when. Innovators or early adopters of smart contract technology will undoubtedly have the market advantage.

A Decentralized Autonomous Organization (DAO) is another potential application. DAOs are created through a bundling of smart contracts. A DAO is an organization, such as a non-profit or corporation, that is organized and operated through software instead of people. While still in a nascent stage of research and development, it’s feasible that buildings or facilities could be organized as DAOs. For example, as a DAO entity, a condominium project with the aid of the internet of things (integration of sensors and meters) could support self-maintenance services, could collect rents through connected digital wallets, could be the platform for tenant voting on building issues, and more.

Finally, blockchain allows for tokenized public finance of public infrastructure, which builds on crowdfunding and P3—but in a blockchain environment that cuts out the friction and costs of traditional bond initiatives. More of the investment money goes directly to projects in need rather than middlemen, and the process is much more transparent and auditable. The first-ever project, in fact, in the United States is expected to be launched by the City of Berkeley through a partnership with Neighborly, an online investment platform.

An added, interesting feature of this blockchain effort is its design for enhanced accessibility, enabling investors to invest directly through the purchase of “mini muni bonds” (see City of Cambridge as case studies), thereby broadening the potential investor pool and democratizing access to wealth-building. The cherry on top for this effort is its economic development structure: If investors desire, interest earned on these bonds may be redeemed through tokens rather than cash—which could be accepted by local retailers and restaurants that might layer on discounts/loyalty rewards.

Predicting future applications that will come from blockchain technology may require a lot of squinting through the fast-paced technical developments and machinations but there’s an important lesson from past history. Back in the mid-1990s, f most didn’t consider how transformative email would become – why would one need to send messages through a computer to one’s colleagues rather than simply walking down the hall and talking with them in person? Hindsight is always 20/20.

With blockchain, the second generation of the internet’s possibilities seem similarly endless. Victor remains vigilant in its research and monitoring and in May 2017 created a Working Group of architectural, engineering, construction industry representatives who will more deeply explore blockchain and ways the technology could ease pain points within the industry. You can follow the Working Group’s activities and stay in touch at https://victorriskmanagement.blog/.

Yvonne Castillo is Vice President of Risk Management for Victor which works with the AIA Trust to offer AIA members quality risk management coverage through the AIA Trust Professional Liability Insurance Program, Business Owners Program, and Cyber Liability Insurance program to address the challenges that architects face today and in the future.